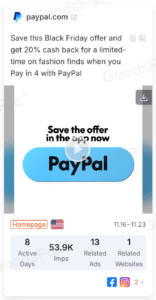

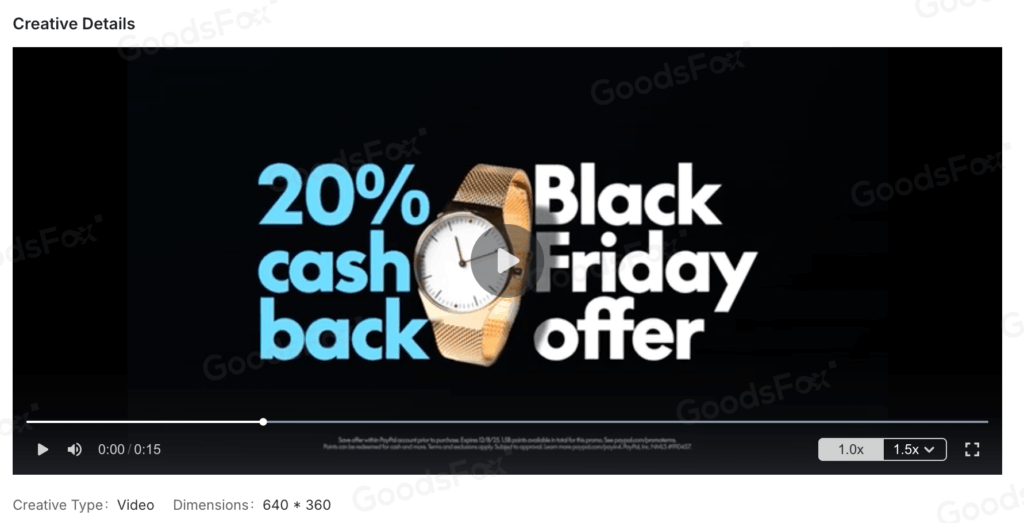

GoodsFox data shows PayPal, the global online-payment giant, is rapidly scaling its BNPL push: ads now run across 49 markets, with creative volume surging 42.8% in 30 days. Most of these ads promote the same message—“Save this Black Friday offer and get 20% cash back for a limited-time on fashion finds when you Pay in 4 with PayPal” This reveals a clear shift: instalments are no longer a side option but a frontline growth strategy.

GoodsFox data shows PayPal, the global online-payment giant, is rapidly scaling its BNPL push: ads now run across 49 markets, with creative volume surging 42.8% in 30 days. Most of these ads promote the same message—“Save this Black Friday offer and get 20% cash back for a limited-time on fashion finds when you Pay in 4 with PayPal” This reveals a clear shift: instalments are no longer a side option but a frontline growth strategy.

source: GoodsFox

Yet the consumers are adopting instalments as routine spending, just as signs of hidden debt and rising delinquencies begin to surface.

BNPL Usage Has Shifted From Convenience to Necessity

Industry veteran Nigel Morris, co-founder of Capital One and early investor in multiple BNPL platforms, recently highlighted a concerning trend: more consumers are now using BNPL to buy groceries. For someone who spent decades analyzing credit risk, this signals that liquidity buffers are evaporating across large segments of the population.

Supporting data tells the same story. BNPL adoption in the United States has surpassed 91 million users, with one in four turning to installment payments for groceries this year—an unmistakable sign that BNPL is filling the gap left by strained credit cards and shrinking savings.

Delinquency Rates Are Climbing

As BNPL becomes more embedded in essential spending, late payments are rising. Delinquencies have increased every year since 2023, underscoring the growing financial stress on lower-income and credit-constrained consumers. Many are no longer using BNPL to optimize cash flow; they’re using it because other options have run out.

Phantom Debt Obscures the True Level of Risk

A more troubling factor is the disconnect between BNPL usage and the traditional credit system. Most BNPL providers do not report loans to credit bureaus, creating what regulators describe as “phantom debt.” Consumers can accumulate multiple loans across platforms, yet lenders cannot see their total exposure. Regulatory data already shows widespread multi-loan behavior, particularly among borrowers with lower credit scores.

A Rapidly Growing Sector With Limited Visibility

The BNPL market is still measured in hundreds of billions, not trillions, meaning it does not yet pose systemic financial risk. However, the combination of rising reliance on BNPL, invisible debt, and a surge in global marketing highlights a structural vulnerability that cannot be overlooked. With economic conditions deteriorating for many subprime borrowers—particularly in auto lending—the actual level of BNPL dependency is likely higher than current datasets suggest.

The Future of BNPL Depends on Transparency and Risk Controls

The convergence of consumer stress, opaque debt accumulation, and aggressive Pay Later expansion places the sector at a critical inflection point. BNPL will remain a core part of digital commerce, but long-term stability depends on improving credit visibility, strengthening oversight, and modernizing risk models to match the industry’s rapid growth.