Ten years ago, global internet usage on mobile devices surpassed desktop for the first time (51.3% vs 48.7%), marking the moment mobile became the world’s primary gateway to the internet. After a decade of explosive expansion, the industry now stands at the beginning of a new chapter. In an era shaped by algorithm-driven feeds — where culture, commerce, and consumer behaviour are increasingly rewritten by digital media — the question is no longer simply where traffic exists, but how ordinary entrepreneurs can still uncover meaningful commercial opportunities within it.

Drawing on global advertising intelligence, AdFox has released the 2026 Global DTC Marketing Insights Report, offering a systematic view of traffic flows, advertising structures, and shifting consumer behaviour across cross-border markets. The report highlights the regions attracting sustained investment, the product categories brands continue to bet on, and the evolving narratives reshaping modern commerce.

This article explores some of the report’s most important findings and core insights.

I. The Global Advertising Landscape Is Becoming More Fragmented

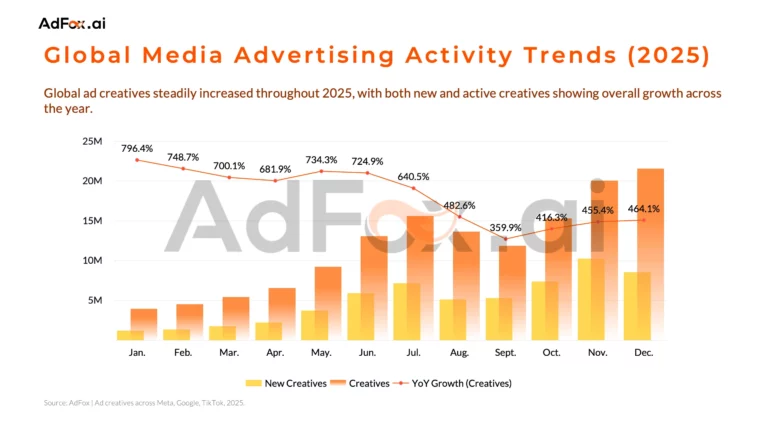

Despite ongoing discussion around a “traffic ceiling”, advertising activity continued to accelerate throughout 2025. According to AdFox data, global media ad volume maintained year-on-year growth, with May recording a striking 734.3% increase. What has truly reached saturation is not traffic itself, but low-cost traffic. Advertising budgets are still rising, yet brands are becoming increasingly anxious about growth as acquisition costs and testing expenses continue to climb.

Against a backdrop of already elevated advertising intensity, 2025 became the year in which the limits of scalable traffic began to emerge more clearly. Active creatives accumulated steadily throughout the year, reaching a peak towards year-end. However, growth was driven less by the influx of new creatives and more by higher-frequency, higher-intensity campaigns from existing DTC sites. The growth rate of active creatives significantly outpaced that of newly launched creatives, signalling a shift from competing through constant novelty to competing within an increasingly crowded stock of existing assets.

Creative lifecycles are therefore becoming noticeably longer, with campaigns running on the same asset for three to six months now increasingly common. In this environment, simply increasing budget allocation no longer guarantees proportional growth. Campaign efficiency is becoming more constrained by inventory saturation and intensifying competition.

January to April — Testing Phase

This period primarily served as a validation window for new markets, products, and storefronts. Both active and newly launched creatives climbed steadily in parallel, reflecting brands testing different market opportunities and creative directions.

May to July — Scaling Phase

The first major inflection point emerged in May and June, as brands began aggressively securing traffic ahead of key promotional periods. By July, seasonal campaigns across multiple regions drove advertisers to scale creatives and markets that had already demonstrated performance.

August to September — Stabilisation Phase

Traditionally a quieter season for global e-commerce, this period lacked major promotional catalysts. Advertisers focused instead on extending the lifespan of existing creatives in order to maintain market visibility while minimising experimentation costs.

October to December — Competitive Phase

Year-on-year growth rates did not rebound significantly during Q4. Beyond the high comparison base from the previous holiday season, this may also suggest that incremental demand had already been pulled forward earlier in the year. With limited expansion on the traffic supply side, competition increasingly shifted away from volume acquisition and towards efficiency and stability.

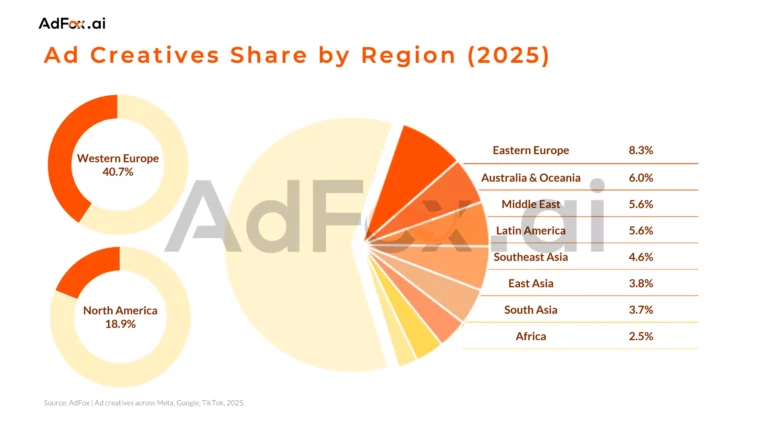

II. Why Western Europe Remains the Core DTC Battlefield

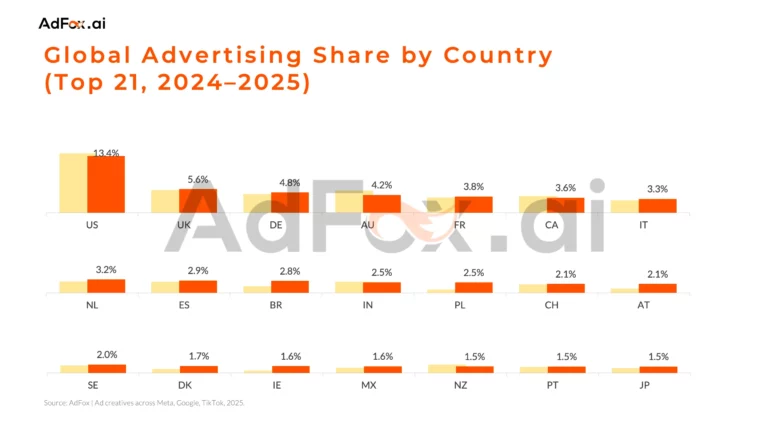

From a regional perspective, Western Europe recorded the highest advertising volume globally in 2025.

Markets such as Germany, France, the United Kingdom, Italy, and Spain together form one of the world’s most mature and stable digital advertising ecosystems. Behind this scale lies highly developed digital infrastructure, strong online shopping penetration, and deeply established consumer brand awareness. Yet Western Europe remains highly fragmented in language, culture, and purchasing behaviour. Regional coverage does not equate to a unified strategy. Localised operations across multiple markets remain essential.

North America, led overwhelmingly by the United States, still accounted for nearly 20% of global advertising volume, underlining its enduring scale advantage. However, beginning in 2025, China’s export reliance on the US market declined significantly amid changing Sino-US tariff policies. Official data shows Chinese exports to the United States falling from US$41.82 billion in April 2024 to US$33.02 billion in April 2025.

At the same time, a number of emerging growth markets are beginning to stand out. Poland’s e-commerce market grew by 9.4%, driven by omnichannel retail and cross-border shopping, and is projected to reach US$37.39 billion by 2030 with a CAGR of 8.59%. Austria’s market reached US$1.345 billion, supported by rapidly growing social commerce activity. Ireland’s e-commerce market climbed to US$631 million, with 74% of consumers planning to increase online spending. Japan’s e-commerce sector expanded by 7.7%, with the market expected to reach US$69.28 billion and digital wallets becoming increasingly mainstream.

Beyond demographic advantages and digitalisation trends, these markets are becoming attractive because their scale is approaching that of several established Western European economies. Meanwhile, consumer spending in these regions has not yet experienced the same degree of pressure from global inflation, leaving brands with fresh room for expansion.

In contrast, Southeast Asia, South Asia, and Africa continue to follow highly platform-centric and socially driven e-commerce models, where independent websites are not yet the dominant format. These regions remain growth-stage markets in which DTC penetration will likely accelerate only as payment systems, logistics infrastructure, and brand awareness continue to mature.

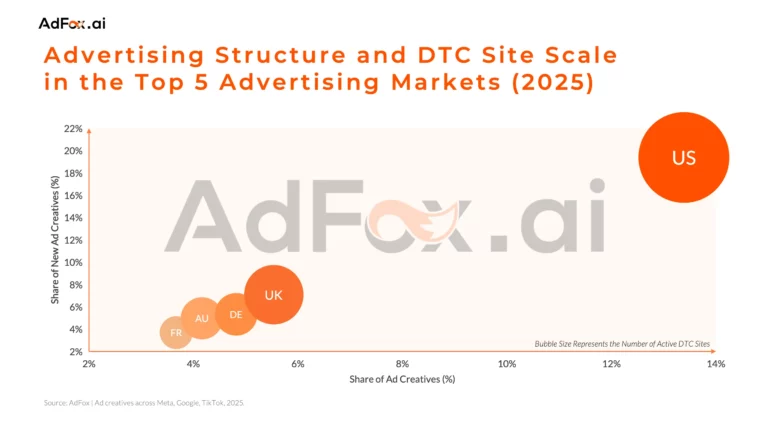

Although the United States is already a mature large-scale market, its advertising cycle remains exceptionally fast-moving. The US accounted for 13.4% of globally active creatives, while newly launched creatives represented an even higher 20.8%. This reflects both the constant influx of small and mid-sized DTC brands and the country’s highly promotional retail calendar. To maintain stable exposure and conversion rates, advertisers must continuously refresh creative assets to combat fatigue. In 2025 alone, more than 760,000 independent websites launched advertising campaigns in the US market, making high-frequency creative testing one of the primary methods for offsetting diminishing marginal returns.

The United Kingdom and Australia, by comparison, resemble more stable expansion markets. The proportion of newly launched creatives slightly exceeded active creatives, suggesting that even within mature DTC ecosystems, incremental growth opportunities remain. As native English-speaking markets, both countries also benefit from stronger efficiencies in creative production, localisation, and cross-market asset reuse, making them among the most scalable expansion destinations outside the United States.

Germany and France present a markedly different profile. While both are highly developed e-commerce markets, their advertising structures appear more stable and conservative. The share of newly launched creatives closely mirrors the share of active creatives, partly because linguistic fragmentation limits the reuse of creative assets across borders. Market size in both countries also correlates closely with population and purchasing power, resulting in growth strategies that prioritise conversion efficiency and longer creative lifecycles over aggressive scaling.

III. Health, Self-Care, and Home Consumption Are Driving Growth

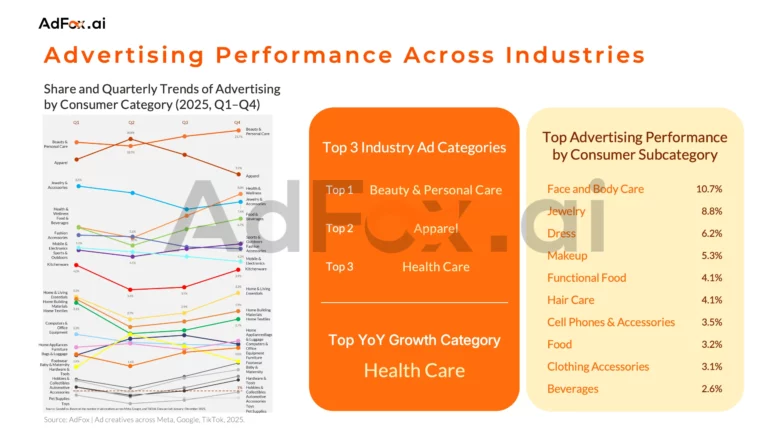

The categories that experienced rising advertising share during Q3 and Q4 2025 — including Beauty & Personal Care, Health & Household, Grocery & Gourmet Food, Sports & Outdoors, Home & Kitchen, Tools & Home Improvement, and Baby Products — generally shared three defining characteristics: high purchase frequency, strong repeat-consumption potential, and close alignment with year-end consumption scenarios.

As the global market entered peak promotional season and household spending intensified in the second half of the year, advertisers increasingly concentrated budgets on categories with stronger conversion certainty and shorter decision-making cycles. These sectors benefited from growing health-conscious lifestyles, holiday gifting demand, and the continued influence of home-centred consumption habits, all of which contributed to stronger advertising efficiency.

In contrast, categories such as Clothing, Shoes & Jewellery, Cell Phones & Accessories, and Pet Supplies saw their advertising share gradually decline from Q2 onwards. Beyond the relative pressure created by faster-growing categories, another key factor was the tightening of small-parcel duty exemption policies across Western markets.

The United States officially removed the “de minimis” tariff exemption for Chinese goods valued below US$800 in May 2025, before expanding the policy globally in August. Import costs for low-value parcels consequently rose sharply, with tariffs ranging between 10% and 30% or fixed fees of US$25–50 per package. This directly squeezed margins for categories heavily reliant on lightweight cross-border parcels, particularly apparel, fashion accessories, and consumer electronics.

The European Union further intensified these pressures by announcing in November 2025 that the €150 duty-free threshold would gradually be phased out from 2026 onwards, beginning with a transitional €3 flat-rate customs charge per parcel from July 2026.

As a result, merchants increasingly reduced investment in lower-priced categories with longer conversion paths, instead shifting focus towards localised supply chains and higher-value product segments.

Overall, Beauty & Personal Care and Health & Household remained the dominant advertising categories throughout 2025, while apparel retained significant scale but faced mounting structural challenges.

Looking more broadly at industry distribution, advertising activity in the second half of 2025 became heavily concentrated within five major sectors: Beauty & Personal Care, Health & Household, Grocery & Gourmet Food, Sports & Outdoors, and Home & Kitchen.

Together, these categories respond to three enduring consumer priorities: health management, self-oriented consumption, and home environment upgrades. Their shared advantages lie in shorter purchasing journeys, stronger repeat-purchase behaviour, and richer storytelling potential within advertising content. Even amid macroeconomic uncertainty, these sectors continue to offer relatively stable conversion performance.

By contrast, traditional high-volume categories such as fashion and accessories continued to lose share. Alongside competitive pressure from faster-growing sectors, tightening cross-border trade policies significantly increased operating costs for low-ticket, lightweight products. Ultimately, the changing advertising landscape reflects a broader shift in consumer preference towards functional value and reliable purchasing outcomes.

IV. Meta Still Dominates — But Discovery Commerce Is Reshaping Consumer Behaviour

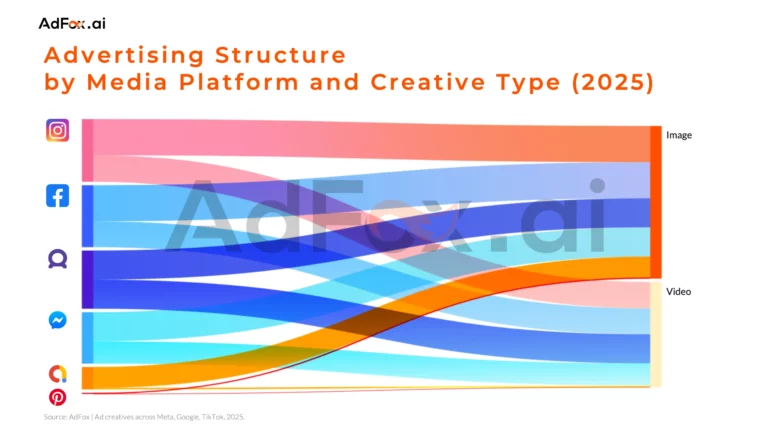

In terms of channel allocation, Meta’s ecosystem — including Facebook, Instagram, and Threads — remained the core advertising battleground for global brands in 2025. This dominance stems not only from sheer user scale, but also from the deeply integrated “social-to-commerce” journey these platforms facilitate.

According to GWI data, 62.8% of users follow or research brands and products on Instagram, ahead of TikTok 56.2% and Facebook 53%. Instagram and Facebook therefore play a critical role in the early stages of the consumer journey, shaping awareness, comparison, and purchase intent before users actively begin searching.

At the same time, another growth path has emerged through platforms characterised by weaker social relationships but stronger discovery mechanisms. TikTok and Pinterest are increasingly reshaping how products are discovered. TikTok’s creator ecosystem and recommendation algorithm continue to redefine impulse-driven commerce, while Pinterest strengthens its position as a visual search and inspiration platform, functioning as an upper-funnel discovery engine.

These shifts are gradually transforming the consumer journey itself — from the traditional “search, compare, purchase” model towards a more instinctive “discover, desire, buy” behaviour pattern. As a result, platform strategy is evolving from simple traffic coverage towards deeper integration within different user-intent scenarios.

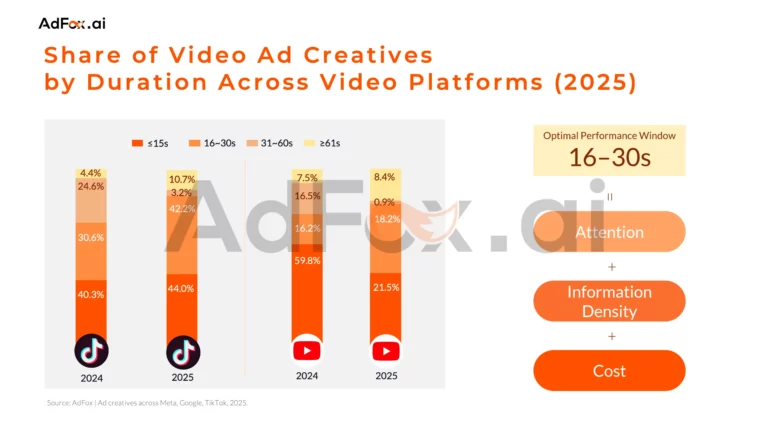

The distinction between TikTok and YouTube ultimately reflects different platform positioning and user psychology. TikTok is built around rapid refresh cycles and algorithmic distribution, where short-form content thrives on immediate feedback loops. YouTube, by contrast, operates as a deeper-content platform centred around search behaviour, subscriptions, and watch time.

Notably, YouTube demonstrated a clear move away from ultra-short advertising formats in 2025. Creatives shorter than 15 seconds fell from nearly 60% of total volume in 2024 to roughly 20% in 2025. This shift appears closely linked to Google’s broader move away from purely exposure-driven Shorts advertising. Across multiple Google Marketing Live events and official YouTube whitepapers throughout 2024 and 2025, the emphasis increasingly shifted from completion rates towards “Effective Attention”.

While ultra-short videos may generate high visibility, they often struggle to support deeper funnel metrics such as brand lift, ad recall, and conversion improvement.

Within this evolving framework, the 16–30 second range has emerged as the most balanced format for video advertising, combining efficiency with effectiveness. From both attention studies and commercial practice, this duration offers sufficient time to move audiences from passive exposure to genuine memorability without substantially increasing production or distribution costs.

More broadly, the evolution of video advertising in 2025 suggests that the industry is moving away from the simplistic assumption that “shorter is always better”. Instead, advertisers are increasingly returning to formats capable of supporting complete storytelling and clearer product communication.

V. Why Vertical Specialist Brands Are Quietly Winning

As the broader market becomes increasingly rationalised, a growing number of specialist vertical brands are demonstrating stronger long-term resilience.

Alongside major players such as HALARA, which continues to scale through highly systematised creative operations, the global DTC advertising rankings also feature niche-focused brands including NRS World equestrian, Milrab skiing, and B.O.C. electric bicycles.

These brands operate within high-barrier, highly specialised niches, building defensible profit pools through product expertise and community-driven engagement rather than competing directly for mass-market traffic. Their common strengths are clear functional positioning, highly defined use cases, and verifiable value propositions — all of which reduce uncertainty in customer acquisition and create more sustainable long-term growth.